Medical debt is surprisingly common in Tennessee, appearing on one in four credit reports. It often results from circumstances tough to predict or control, and even small amounts can make it harder to get ahead. However, there are many options for policymakers who want to prevent medical debt, help people manage their medical bills, and mitigate medical debt’s negative effects on financial security, economic mobility, and health.

Prior reports provide important background on how medical debt occurs, how it affects people’s lives, and who has it in and across Tennessee. For those in a hurry, we also have a one-stop summary and infographic of all our medical debt analysis to date.

Key Takeaways

- The complexities of medical debt offer policymakers a wide range of opportunities to prevent the problem, help people manage it, and mitigate its effects.

- Prevent: Upstream policy levers that address surprise bills, access to coverage, and out-of-pocket insurance costs could help prevent many situations that cause medical bills to go unpaid.

- Manage: Midstream options that address provider billing, personal savings, and access to financial capability services and affordable, small-dollar lending could help make medical bills easier to manage.

- Mitigate: Downstream policy options that affect debt collection practices and lawsuits, risky debt settlement services, the use of credit history, and debt pay-off could help to mitigate the negative effects of medical debt.

- There is no silver bullet for medical debt. While some options listed here may have more impact than others, none would address every aspect of the problem by themselves.

Acknowledgement: This research was funded by the Annie E. Casey Foundation. We thank them for their support but acknowledge that the findings and conclusions presented in this report are those of the authors alone, and do not necessarily reflect the opinions of the Foundation.

Sycamore takes a neutral and objective approach to analyze and explain public policy issues. Funders do not determine research findings. More information on our code of ethics is available here.

Overview

There are a range of state-level policy levers available to address medical debt and its effects on Tennesseans. While not necessarily an exhaustive list, this report summarizes 12 potential areas that state policymakers may want to explore (Figure 1). The full report discusses each option in more detail, including its trade-offs, the causes and effects of medical debt that it targets, and other key considerations.

Our research suggests no single policy change would address every troubling aspect of medical debt in Tennessee and its downstream effects. For example, getting more people enrolled in health insurance would make new medical debt less likely among those currently uninsured, but it would not affect existing debts or curtail surprise out-of-network bills for those with insurance. Tennesseans incur medical debt for many reasons, including circumstances that may be tough to predict or control, and the downstream effects on financial stability, economic mobility, and health range widely. Each option presented here addresses different aspects of this problem.

Not all policy options are created equal. Each one involves trade-offs, and some options may have more impact than others based on the specific causes and effects across Tennessee. The evidence also suggests that some options are more proven than others at achieving the intended goal. For example, health care price transparency efforts have long held the promise of lowering patients’ out-of-pocket spending, but many experiments in this area have come with unintended consequences or fallen short of expectations.

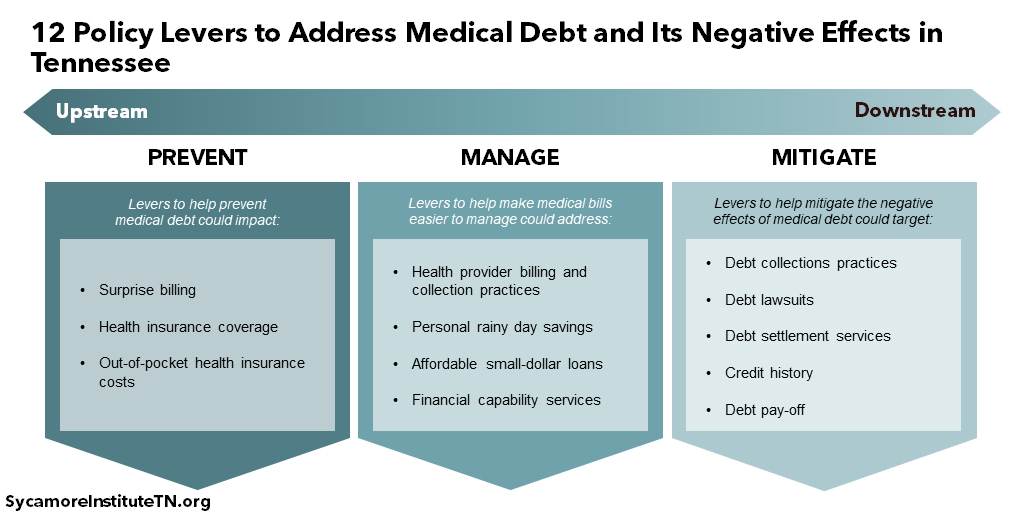

Figure 1

Upstream Options to Prevent Medical Debt

Upstream policy levers seek to prevent many situations that cause medical bills to go unpaid. Policies in this area could impact:

- Surprise Bills — Curtailing surprise bills may help prevent medical debts that result from unexpected bills when patients visit in-network or emergency facilities but get treated by out-of-network providers. Policymakers could require insurers to pay out-of-network providers a predetermined or arbitrated rate, or they could regulate how providers bill patients and/or contract with insurers.

- Health Insurance Coverage — Getting more Tennesseans enrolled in health insurance could help those individuals to better afford health care services and avoid medical debt. For instance, a state reinsurance program could make some private plans more affordable. Another example is exploring ways to address delays, lapses, and gaps in coverage for low-income Tennesseans.

- Out-of-Pocket Health Insurance Costs — Offering patients tools to minimize their out-of-pocket health insurance costs could help prevent medical debt by making some medical bills more affordable. High out-of-pocket insurance costs may mean that even insured individuals end up with unpaid medical bills. Reducing out-of-pocket costs could be challenging, but some states have explored using price transparency measures as a way to help patients better shop for health care.

Midstream Options to Manage Medical Debt

Midstream policy approaches aim to help make medical bills easier to manage. These include efforts to address:

- Provider Billing and Collection Practices — Changing provider billing and collection practices could help prevent, manage, and mitigate medical debt. For example, new rules and oversight could facilitate patients’ access to financial assistance, payment plans, or insurance coverage for which they might be eligible. It could also shed light on providers’ use of extraordinary collection practices (see Debt Lawsuits).

- Personal Rainy Day Savings — Facilitating and incentivizing personal savings could reduce debt and promote financial stability by helping Tennesseans use their own resources to better weather unexpected expenses. For example, connecting Tennesseans without bank accounts to traditional financial services could remove obstacles to saving when funds are available.

- Affordable, Small-Dollar Loans — Increasing access to affordable, small-dollar loans could help some individuals to better manage unexpected medical expenses and avoid a cycle of debt. Alternative financial products like payday loans can be expensive but help people fill income gaps or pay for unexpected expenses like medical bills. Policymakers could explore ways to make these kinds of resources available at a lower cost to people who rely on them.

- Financial Capability Services — Improving access to services like financial literacy classes and one-on-one counseling and coaching could help people prepare for and manage debt if and when it occurs. For example, both Memphis and Nashville support financial empowerment centers that provide one-on-one financial counseling for people with low-incomes. Available data show that Nashville’s center has improved financial outcomes for its clients.

Figure 2

Downstream Options to Mitigate Medical Debt

Downstream policy options could help mitigate the negative effects of medical debt. Unpaid medical bills can become indistinguishable from most other types of consumer debt once they are purchased by a debt buyer (Figure 2). For this reason, many of the downstream options address debt generally or offset the negative effects of bad debt. Actions in this area could affect:

- Debt Collection Practices — Reining in some debt collection practices could improve debt repayment outcomes and reduce debt-related stress among Tennesseans with unpaid medical bills. Policymakers could explore ways to revise existing rules for debt collectors, like expanding to whom the rules apply, limiting interest rates, and including new modes of communication.

- Debt Lawsuits — Addressing certain aspects of debt collection lawsuits could reduce some of the negative financial and legal fallout from medical debt. For example, national research suggests that many of these lawsuits go unchallenged. Policymakers could look at ways to expand access to legal representation or support tools for people to represent themselves.

- Debt Settlement Services — Greater oversight of debt settlement services could protect people looking for manageable ways to pay off their debts. Existing law provides protections for consumers using these services, but national cases show that many companies continue to engage in fraudulent practices. Tennessee policymakers could explore ways to add more protections while expanding access to less risky services like financial counseling.

- Credit History — Limiting how medical debt affects a person’s credit history could address a potential significant obstacle to their financial stability and economic mobility. For example, state law already excludes medical debt from the information that can be used to set home and auto insurance terms and premiums. State lawmakers could consider additional limits for when medical debt can be reported to a credit bureau and how medical debt-related credit history information can be used.

- Debt Pay-Off — Paying off debts directly could reduce financial burdens on affected individuals and improve their economic security, potentially for less than the debt’s face value. For example, one national nonprofit uses charitable donations to buy and forgive resold medical debt for low-income and financially insecure individuals.

Parting Words

Each policy option could help improve Tennesseans’ financial security, economic mobility, and health by addressing one or more aspects of medical debt. The complexities and unique features of medical debt mean there is no single answer that addresses every aspect of the problem and its downstream effects in Tennessee. As policymakers consider the details of each strategy as discussed in the full report, they will have to balance the trade-offs and potential for unintended consequences inherent in every public policy decision.

Read the full report for a more in-depth analysis and a full list of sources and citations.