Key Takeaways

- The FY 2023 budget amendment adds $260 million in net new spending from state revenues.

- In total, it proposes $316 million in new expenditures and $100 million in new tax cuts – offset by changes that increase revenues and reduce funding for items proposed in February.

- It does not fundamentally change tax collection forecasts or the use of recurring revenues for nonrecurring expenses – despite collections seven months into the current fiscal year being on a safe path to meet February’s updated projection.

This week, Governor Lee proposed an amendment to his budget recommendation for FY 2023, which starts July 1, 2022. These revisions update the original budget plan the governor rolled out in February, reflecting new information about program needs and legislative action. With these changes, the FY 2023 budget recommendation now totals $52.8 billion[i]– including $26.6 billion from state revenues. (1) (2) (3) (4)

The administration amendment marks one of the final steps in the process to get next year’s budget approved by the legislature (which will likely be one of the General Assembly’s final actions before adjourning for the year).

Overview

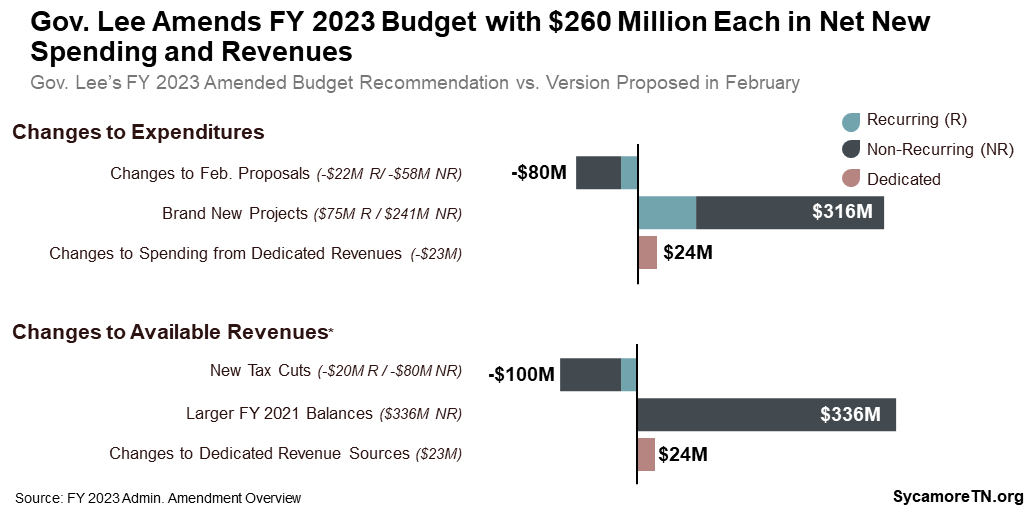

The amended FY 2022 proposed budget includes $26.6 billion from state revenues – $260 million higher than before – which includes annual costs of new debt for a Titans stadium. These net increases are the combined result of dozens of changes that affect both revenues and expenditures (Figure 1). Here are the topline differences with the February recommendation.

Expenditures

- Changes to February Proposals – Net reduction of $80 million in spending ($58 million recurring and $22 million non-recurring) on programs and legislative initiatives proposed in February.

- Brand New Projects – Increase of $316 million in spending ($241 million recurring and $74 million non-recurring) for brand new initiatives and capital projects.

Revenues

- Tax Cuts – Reduction of $100 million in revenue ($20 million recurring and $80 million non-recurring) from permanent and one-time tax cuts.

- Larger FY 2022 Balances – $336 million in additional funds carried over from the current year as non-recurring revenue for use in FY 2023.

The sections that follow highlight significant items in each of these areas.

Figure 1

Changes to February Expenditures

The governor’s amended budget re-estimates the costs of some of the initiatives proposed in February – freeing up a total of $80 million ($23 million recurring and $58 million non-recurring) for other purposes. This includes:

- Reconciling Budget and Fiscal Note Cost Estimates – $30 million in net non-recurring savings comes from adjusting the budget’s initial cost estimates for certain activities to match estimates by the legislature’s Fiscal Review Committee. The largest of these reductions are $18 million for a bill related to foster care for young adults ages 18-21 and $7 million for recognizing Juneteenth as a state holiday.

- Reductions to Requested Increases – $20 million in net savings ($12 million recurring and $8 million non-recurring) from scaling back some of the increases proposed in February. The largest of these is a $12 million to recurring reduction a proposal related to graduate medical education, which is now proposed at $10 million.

- Administration Amendment Placeholder – $30 million reallocation ($10 million recurring and $20 million non-recurring) from a placeholder in the original budget to help fund new initiatives not included in the February request.

Brand New Spending

The amended budget includes a total of $316 million in new FY 2023 spending – including $74 million recurring and $241 million non-recurring. The largest of these go towards earmarked grants, airports, and the construction of a new Titans stadium in Nashville.

Earmarked Grants

The revised budget proposes $85 million ($4 million recurring and $81 million non-recurring) for 77 targeted grants to specific communities and organizations. The largest grants include $20 million to the city of Memphis for riverfront development and $10 million to the National Civil Rights Museum in Memphis. Another 21 grants are $1-4 million, and the remaining 54 range from $11,500 to $760,000 apiece.

Airport Subsidies

The amended budget includes a $78 million one-time General Fund transfer to the Transportation Equity Fund for airports. Of this, $66 million would support the state’s five large commercial service airports in Memphis, Nashville, Knoxville, Chattanooga, and the Tri-Cities. The other $12 million would go to 69 general aviation airports. Airports can use the funds for a variety of activities – including repairs and construction, land acquisition, and safety and security upgrades. (5)

Lawmakers approved both one-time and recurring transfers for FY 2022 for the same purpose to replace a decline in revenues from the dedicated funding source for airports. In 2021, the General Assembly approved a one-time $50 million transfer and a $3 million recurring subsidy that began in FY 2022. Historically, the state’s aviation fuel tax has supported state funding for airports. Lawmakers capped and cut that tax in recent years, which led to a drop in the program’s dedicated funding. (6) (7)

Titans Stadium

Gov. Lee proposed $55 million in recurring debt costs for $500 million in bonds to subsidize construction of a new, covered stadium for NFL games and other events. Metro Nashville and the Tennessee Titans are in talks to renovate or replace the current 23-year-old, open-air stadium and develop the surrounding land (mostly parking lots). These funds would only be available for a new, enclosed stadium, which could reportedly cost an estimated $2 billion. Once complete, the project might bring more large events to Nashville – such as wintertime concerts and major sporting events. The state approved a separate subsidy last year when talks focused on renovating the current stadium. Cost estimates to renovate have since climbed, and the mayor now appears focused on building a new venue. (8) However, the city and the Titans have not yet made any official agreements.

The state of Tennessee is still paying off its original investment in the current stadium. In 1996, the state approved a $55 million contribution to the $264 million construction of the Titans’ stadium, which was completed in 1999. (9) (10) (11) The state funded its contribution by selling bonds. Those bonds are being paid down with state sales tax collected at the stadium during Titans-related events and will be fully paid off in FY 2029. (12) Through FY 2021, state sales tax collections for other events at the stadium went to the state General Fund like normal.

Last year, lawmakers approved a new 30-year state tax subsidy for the stadium renovation and development. Under the 2021 law, the state will continue to retain enough of the state sales tax collected at the stadium to finish paying off its original $55 million debt through FY 2029. Nashville’s Metropolitan Sports Authority now keeps the rest (estimated at about $2 million per year) and half of the state sales tax collected within a 130-acre area around the stadium for up to 30 years to offset the costs of new renovations, construction, and development. (13) The cost estimate for the 2021 law speculated that the state’s foregone revenues for new activity on the surrounding land could amount to $10 million a year – depending on extent of redevelopment and future economic activity in the area. (12)

Tax Cuts

The governor’s amendment reduces revenues by $100 million with a new permanent tax cut and a temporary grocery tax holiday. Details are as follows:

- Grocery Tax Holiday – The amendment proposes a one-month grocery sales tax holiday. This would cost the state a total of $80 million – including $49 million for the state’s 4% grocery tax and about $31 million to reimburse local governments for lost local option sales tax.

- Professional Privilege Tax Reduction – A cut to the professional privilege tax from $400/year to $300/year would reduce revenues by an estimated $20 million per year. The tax currently applies to lobbyists, physicians, attorneys, securities agents, broker-dealers, and investment advisors. Over three-quarters of those who currently pay the tax live out-of-state.(14) In 2019, lawmakers exempted 15 professions previously subject to the tax. Governor Lee has twice proposed reducing the tax for the remaining professions, but those proposals were shelved first by the pandemic in 2020 and then by the General Assembly in 2021.

Larger FY 2022 Balances

The amendment proposes additional changes to the current-year balance that would boost the estimated funds available for FY 2023 to $4.7 billion, an increase of $336 million. These funds will become non-recurring revenue for FY 2023. The increase is the net result of changes that free up available dollars and increase FY 2022 spending for two purposes. Highlights include:

Increases in Available FY 2022 Dollars

- Unspent Appropriations – $211 million from unspent program funds that revert back to the General Fund. This includes $170 million from normal agency underspending, $16 million in unspent funds for state employee retirement buyouts, and $25 million savings from the education savings account program. Non-recurring spending reductions of this kind are known as reversions. End-of-year program reversions are common and typically total about $150-200 million per year.

- Broadband Infrastructure – $100 million previously appropriated for broadband infrastructure grants. The governor proposes forgoing the General Fund investment because federal dollars are available for the same purpose. The state has reserved $500 million of its American Rescue Plan dollars for broadband expansion and adoption.(15)

Increases in FY 2022 Supplemental Spending

- Gas Expenses – $5 million to cover higher gasoline cost for state agencies.

Tax Projections

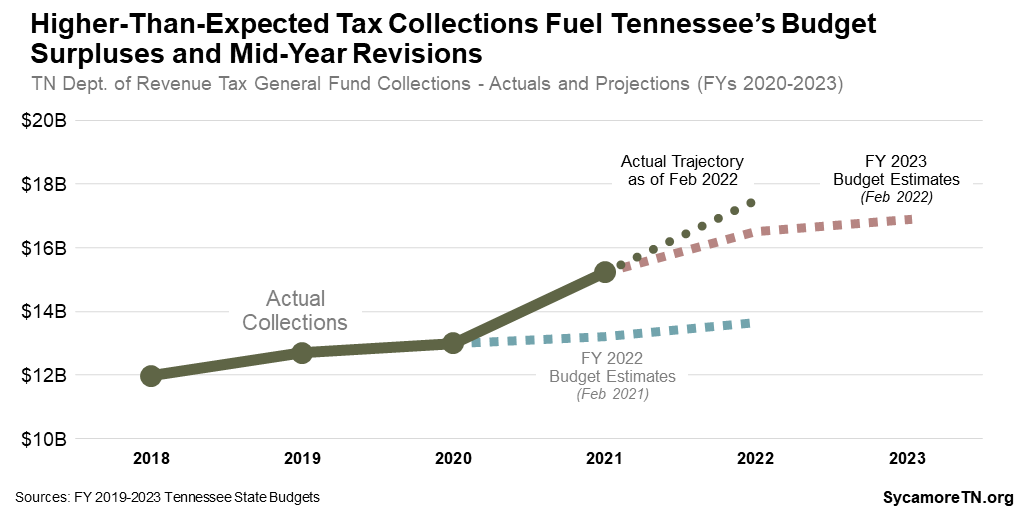

Tax collection forecasts for FY 2022 and FY 2023 remain unchanged, and the amendment continues using $1.3 billion in recurring growth to support non-recurring investments (see our February summary for more details). The plan Gov. Lee proposed two months ago assumes the state will collect $3.0 billion more in FY 2022 than is currently budgeted – including $2.9 billion in the General Fund. This assumption also grew the FY 2022 base budget by the same amount (Figure 2). Seven months into the current fiscal year, actual collections are about $2.1 billion more than is currently budgeted and are on track to be $3.9 billion more by the end of the fiscal year – including $3.8 billion in the General Fund (Figure 2). (16)

Figure 2

[i] Does not include the $500 million bond authorization for a new Titans stadium. Bond authorizations are typically counted in the “other” category of the state budget, but the $500 million was not included in the totals presented by the Commissioner of Finance and Administration to the General Assembly. We have excluded it here to ensure that totals match with official estimates.

References

Click to Open/Close

- Tennessee Department of Finance and Administration. FY 2022-2023 Administration Budget Amendment Overview. March 28, 2022. https://www.tn.gov/content/dam/tn/finance/budget/documents/overviewspresentations/23%20Admin%20Amend%20Overview%204.3.pdf

- —. Commissioner’s Presentation – FY 2023 Budget Amendment. March 29, 2022. https://www.tn.gov/content/dam/tn/finance/budget/documents/overviewspresentations/FY23%20Budget%20Amendment%20Presentation%20-%20FINAL.pdf

- Senate Finance, Ways, and Means Committee. Hearing on FY 2023 Budget Amendment. Tennessee General Assembly. March 29, 2022. Video recording at https://tnga.granicus.com/MediaPlayer.php?view_id=614&clip_id=26760

- House Finance, Ways, and Means Committee. Hearing on FY 2023 Budget Amendment. Tennessee General Assembly. March 29, 2022. Video recording at https://tnga.granicus.com/MediaPlayer.php?view_id=636&clip_id=2676

- Tennessee Department of Transportation. Transportation Equity Fund Report for FY 2020-2021. December 2, 2021. https://www.tn.gov/content/dam/tn/tdot/finance/FY%202020-2021%20Transp%20Equity%20Fd%20Report-DOT.pdf

- Styf, Jon. Tennessee’s Airports Seek $125M in New Annual Funding. The Center Square. January 27, 2022. https://www.washingtonexaminer.com/politics/tennessees-airports-seek-125m-in-new-annual-funding

- State of Tennessee. Tenn. Code Ann. § 67-6-217.

- Stephensen, Cassandra and Mazza, Sandy. Nashville Is Looking At Up To $2 Billion For a New Football Stadium. The Tennessean. February 28, 2022. https://www.tennessean.com/story/news/local/davidson/2022/03/01/nashville-new-football-stadium-2-billion/6943679001/

- Metropolitan Government of Nashville & Davidson County. Nissan Stadium. [Online] [Cited: March 30, 2022.] https://www.nashville.gov/departments/sports-authority/nissan-stadium

- State of Tennessee. Proposed Capital Appropriations from Bonds, Current Funds and Other Revenues, FY 1996-97 (pA-73). FY 1996-1997 Tennessee State Budget . 1996.

- —. Public Chapter No. 582 (1996). Accessed via Tennessee Legislative Services. .

- Fiscal Review Committee Staff. Fiscal Memorandum: SB 1543-HB 1437. Tennessee General Assembly. [Online] March 22, 2021. https://www.capitol.tn.gov/Bills/112/Fiscal/FM0622.pdf

- State of Tennessee. Public Chapter No. 401 (2021). https://publications.tnsosfiles.com/acts/112/pub/pc0401.pdf

- Fiscal Reveiw Committee Staff. Fiscal Note: SB 2524-HB 2776. March 7, 2022. https://www.capitol.tn.gov/Bills/112/Fiscal/SB2524.pdf

- Tennessee Department of Finance and Administration. Financial Stimulus Accountability Group. March 23, 2022. https://www.tn.gov/content/dam/tn/finance/documents/financial-stimulus-accountability-group/032322March.pdf

- —. February Revenues. March 11, 2022. https://www.tn.gov/finance/news/2022/3/11/february-revenues.html